Looming Electrical Grid-lock

Back in 2019-2020, we were doing research on electric vehicle-as-an-amenity company called Envoy (sold to Nasdaq: BLNK in 2022). The company essentially provided EVs to condo buildings for the residents to use as an amenity. During that research, we spent quite a bit of time looking at the projected EV adoption curve (largely driven by government incentivization) and the potential for unintended strain on regional electric grids. Indeed, many pundits and researchers expressed serious concerns around this issue at the time (links 1, 2, 3, 4). To reach many of the medium-term electrification targets policy makers were clamoring for, grid capacity in the US would have to effectively double, requiring trillions of dollars of investment within +/- a decade.

From a practical standpoint, this was clearly unrealistic, making these massive energy infrastructure upgrades a bottleneck for exponential demand upticks. It seemed that those “all-in” on electrification were making a big bet: either collection/battery technology would materially improve or that the EVs themselves would be able to act as a defacto distributed energy grid, capable of using, storing, and distributing energy among themselves. Both require decoupling time of production from time of use via storage. Certainly not impossible but also not without significant risk. Side note: we were fascinated by the idea of a distributed EV-driven grid system and we did end up making the investment in Envoy in 2020.

Fast forward to 2024. EV demand is still growing at very solid clip (a record 1.2 million EVs were sold in the US in 2023, up about 30% YoY) and there are now more than 4 million EVs on American roads. Great news. But we have also seen noteworthy and expectant cracks emerge in our grid systems and the most promising battery storage tech is not ready for “primetime.”

Now a new and much more important threat to the promise of sustainable electrification has emerged: AI. Turns out, the chips that are powering the AI revolution require a lot of power. Moreover, the power they require is baseload power, power that can’t easily be sourced via renewables. Estimates suggest that a single Nvidia 100 series chip consumes about 2/3rd the power of an average single-family home. Given that +3 million of these chips are forecast to be shipped in 2024, that’s the equivalent of adding a city roughly the size of Toronto in a single year!

This is INCREMENTAL energy demand that was not even on the radar 24 months ago, and the spike has caught the world by surprise:

“The world adds a new data center every three days” (link)

“The five-year projection of U.S. electricity demand growth has doubled from a year ago, according to a report from consulting firm Grid Strategie” (link)

“EirGrid in Ireland estimates that electricity demand from data centers could more than double to 30% of all consumption in 2028” (link)

“In Denmark, electricity usage from data centers is forecast to grow from 1% to 15% of total consumption by 2030.” (link)

These projections are astronomical. Add to this increased restrictions (pushing electrification) on gas stoves, HVAC systems, etc. and we have all the makings of a potentially very dangerous energy crisis. Incremental improvements on the collection/battery side will obviously help, but big needle movers such as small scale nuclear (or even just the aggressive roll-out of traditional nuclear) are decades away.

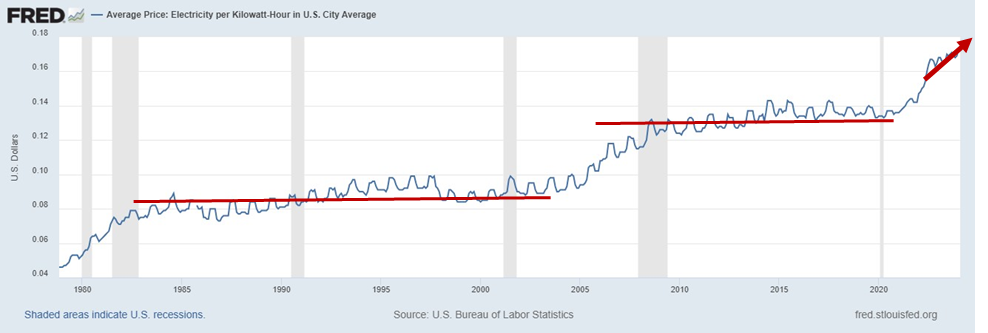

What might this mean financially for the average (already strapped) homeowner that has already seen prices jump materially since 2020?

What might this mean for policies and incentives around “electrifying America” and home innovation in general?

For now, our simple thesis is that policy makers will conclude that we need more of virtually all types of energy and will be forced to embrace material natural gas expansion in the short-term while accepting nuclear over the medium term. When it comes to AI, the toothpaste is out of the tube - there’s no going back.

Rather thinking of it as step backwards in terms of our renewable energy transition, we see it as an opportunity to build up more electrification infrastructure in and around the home safely. Ramping up current methods of energy production will allow the pace of adoption of home electrification to proceed its steep upward trajectory, and lay a groundwork of customers to transition to new methods of energy production over time. From there, the dreams of full electrification, digitization, and optimization are possible at a mass scale. It also gives bandwidth for energy storage technologies to become market ready. Any alternative would be to risk constricting the energy supply and force the grid’s hand into breakdown – and the ones that will hurt the most from rolling blackouts likely won’t be the ones with Teslas in the garage.

A decade of mutual compromise followed by a higher efficiency forever is a more exciting picture than an eternity of electrical gridlock.